Track mileage automatically

Get startedSelf-Employed Mileage Deduction Rules

In this article

- Who is this guide for?

- How much do people claim on taxes on average?

- Trips that count as business mileage

- Trips that are NOT considered business mileage

- Choose between two deduction methods

- Standard mileage rate method

- Actual expenses method

- Records you need to keep

- How to calculate your 1099 mileage tax deductions

- What the deduction actually saves you

- Mileage tracking and your quarterly estimated taxes

- Other circumstances for workplaces and vehicle ownership

- FAQ

- Who is this guide for?

- How much do people claim on taxes on average?

- Trips that count as business mileage

- Trips that are NOT considered business mileage

- Choose between two deduction methods

- Standard mileage rate method

- Actual expenses method

- Records you need to keep

- How to calculate your 1099 mileage tax deductions

- What the deduction actually saves you

- Mileage tracking and your quarterly estimated taxes

- Other circumstances for workplaces and vehicle ownership

- FAQ

Who is this guide for?

As a self-employed person, you might be eligible for a tax deduction on all your business-related driving. This guide is for you if you’d like to know how to claim mileage on taxes and you’re struggling to navigate self-employed mileage deductions. You’re likely one of the following:

- A small business owner who reports their income on Schedule C form

- A freelancer

- An independent contractor

Follow along to find out how much tax money people like you claim on average, what’s considered business mileage, and the rules and limitations to claiming your tax deductions from the IRS.

As of 2026, the mileage deduction is exclusively a self-employed benefit. The One Big Beautiful Bill Act (OBBBA), signed into law in 2025, permanently eliminated the ability for most W-2 employees to deduct unreimbursed mileage on their personal tax returns — a suspension that was previously expected to expire.

Mileage tracking made easy

Trusted by millions of drivers

Automate your logbook Automate your logbook

Automatic mileage tracking and IRS-compliant reporting.

Get started for free Get started for freeHow much do people claim on taxes on average?

Since there’s no upper limit to how many miles you can claim, self-employed tax deductions vary wildly from person to person and depend mostly on the cost of the car, how new it is, and how much you drive.

For average business miles claimed on taxes here at Driversnote, we see everything from a few hundred business miles a year to tens of thousands, with the average mileage claim by the standard mileage rate method sitting at around $5,500 for self-employed actively driving for an entire year.

Example: Let's say you drove 2,000 miles for business in 2025. To calculate your mileage tax deduction, multiply the 2025 mileage rate by your business miles: 2,000 miles × $0.70 = $1,400 in mileage deductions. For the first half of 2026, the same 2,000 miles would give you: 2,000 × $0.725 = $1,450. Effective July 1, 2026, the rate has gone up to $0.76. That means if you drive 2,000 miles in the second half of the year, you'll be able to claim $1,520.

Claims tend to go higher for those using the actual expenses method.

As to the types of drivers that log the most miles, gig workers such as rideshare drivers and delivery couriers are currently among the most prolific drivers in the U.S.

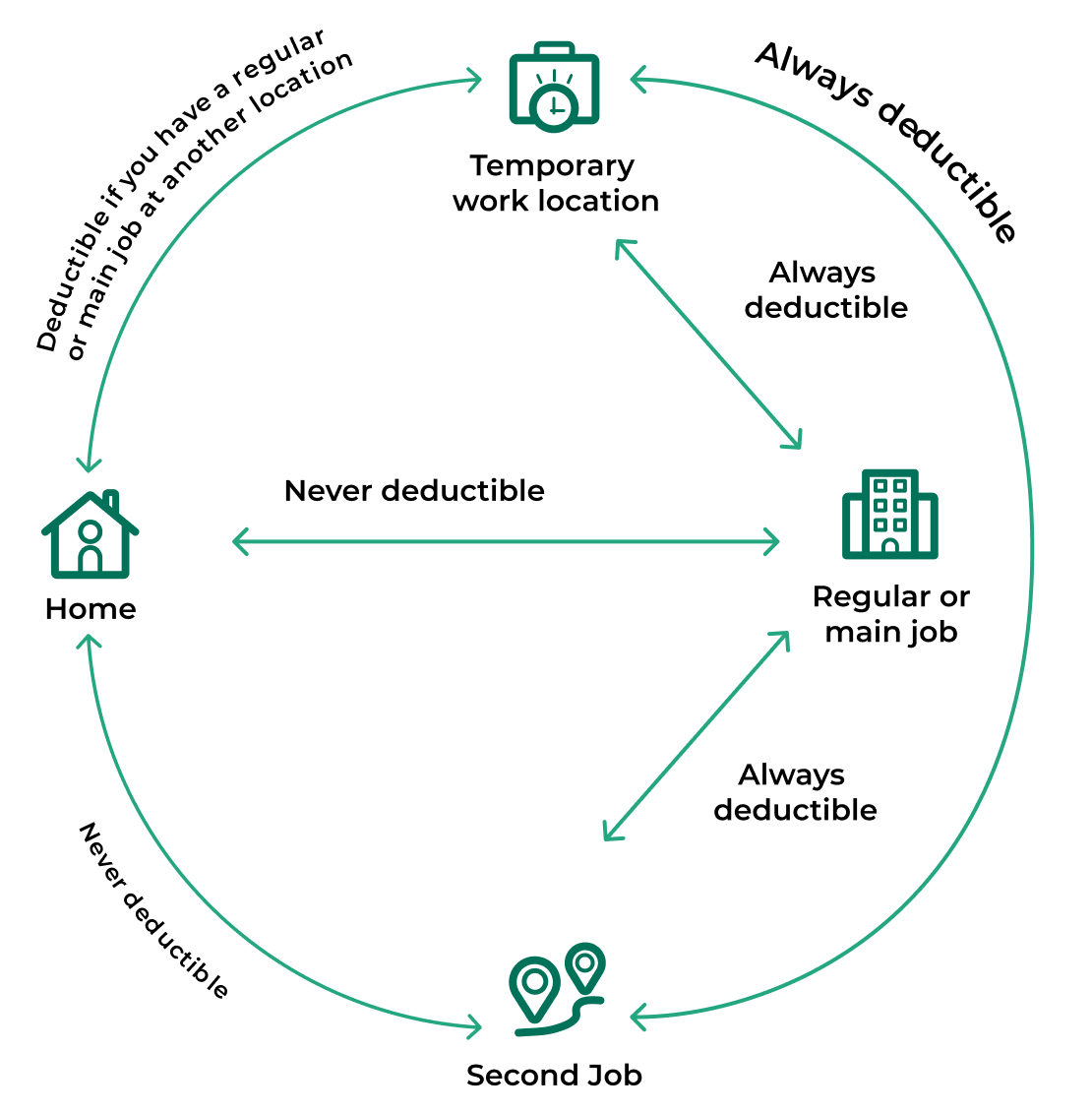

Trips that count as business mileage

The IRS classifies the following trips as tax-deductible:

- Driving between two different workplaces

- Driving from your home to a temporary workplace (a workplace is generally defined as temporary if you expect to work there for less than one year)

- Meeting clients and visiting customers

- Running business-related errands

Trips that are NOT considered business mileage

The types of trips that aren’t considered business (but you still might need a record of; see below for record-keeping):

- Commuting to and from your home to your permanent workplace

- Commuting to and from your home to a second workplace

Home office exception: If you have a home office that qualifies as your principal place of business, the commute rule works differently. Driving from your home office to any other business location — a client site, a co-working space, a supplier — counts as a business trip, not a commute. See the "Other circumstances" section below for the full rules.

Here's an overview of the trips you can take to and from work:

Hauling tools or displaying advertisements is not considered business mileage

Aside from commute not being deductible, hauling tools or instruments when commuting doesn’t make it a business trip and, therefore, remains non-deductible (classified as personal use); the same applies to displaying advertisements on the car. These are both common misconceptions.

Choose between two deduction methods

There are two methods for calculating your 1099 mileage deduction, each with its own set of rules and limitations for deducting business mileage as self-employed.

You must choose between the two, and your choice in the first year of using your car for business often affects your options later. One applies the IRS standard mileage rate, and the other lets you deduct the actual expenses related to owning and operating the car.

Standard mileage rate method

The standard mileage rate method uses a set IRS rate you can apply to calculate tax deductions per business mile driven.

This method is more straightforward than working out actual expenses, as the rate covers all expenses of owning and running your vehicle for business purposes.

With the 2026 IRS mileage rate, you can claim $0.76 per mile for business-related driving ($0.725 in the first half of 2026). The 2025 IRS mileage rate is $0.70 per mile, applicable from January 1, 2025, until December 31, 2025.

When you opt for the standard mileage rate method, you can deduct an amount per mile driven, along with tolls and parking fees incurred for business purposes. Commuting is generally non-deductible, but read on for details.

Qualifying for the standard mileage rate method

To qualify for the IRS standard mileage rate method, you must own or lease the car(s) you drive for business. Depending on whether you do one or the other, there are different criteria for eligibility.

You own the car

If you want to use the standard mileage rate, you must choose it in the first year of the car’s operation in your business. In later years, you can switch to actual expenses (for specifics, check switching below).

However, this method is NOT available if you:

- Claimed depreciation deductions on the car (other than the straight-line method)

- Claimed a section 179 deduction or the car's Special Depreciation Allowance

- Simultaneously use five or more vehicles for your business (fleet operations); however, you may switch between the vehicles

- Are a rural mail carrier who receives a qualified reimbursement

You lease the car

When leasing, you must commit to the standard mileage rate method for the entire lease period.

This method is NOT applicable if you:

- Simultaneously use five or more vehicles for your business (fleet operations) - however, you may switch between the vehicles

- Claimed actual car expenses for a leased car after 1997

Actual expenses method

As a self-employed person, you can claim deductions for expenses related to owning and operating a vehicle for business purposes. The IRS identifies deductible expenses as:

- Depreciation or rental and lease payments

- Gas and oil

- Tires

- Repairs

- Insurance

- Registration fees

- Licenses

- Parking fees and tolls*

- Garage rent

- Trailer rental costs (when hauling tools or instruments)

- Interest payments on your personal car loan

*If you use the standard mileage rate, you can still deduct parking fees and tolls.

Depreciation might disqualify you from using the standard mileage rate method

There are three types of depreciation that, if taken, might disqualify you from switching to the standard mileage rate method:

- The Section 179 Deduction

- The Depreciation Deduction

- The Special Depreciation Allowance

We recommend you read up on depreciation in the IRS’s publication or consult your tax professional.

Tips for choosing the right method for you

The actual expenses method generally requires more work since you have to maintain more records. But, it might come with financial benefits based on your circumstances, namely the cost of your car and how expensive it is to run.

You should look into the actual expenses method, if:

- Your car is worth more than average

- Your car is more costly to operate and maintain than average

The standard mileage rate for business is based on a national average and uses straight-line depreciation. If you’ve bought a new or expensive car - which generally depreciates more during its first years of service - it’s likely that you can deduct more tax via depreciation by using the actual expenses method.

Again, don’t choose before calculating your deduction using both methods. We also recommend that you ask your tax professional for help.

For a side-by-side comparison of both methods with a worked example, see our standard mileage vs actual expense guide.

Switching between the methods

If you choose to use the actual expenses method in the first year your vehicle is available for use in your business, you won’t be able to apply the standard mileage rate method in any following year while you drive that vehicle.

However, if you use the standard mileage rate method in the first year, you can choose between the two methods in the following tax years. Be aware of how you calculate your depreciation, as it might affect eligibility for the standard mileage rate method.

As mentioned earlier, if you want to use the standard mileage rate for a car you lease, you must do so throughout the entire lease period and any lease extensions.

Records you need to keep

For the standard mileage rate method

You must keep a timely log of your business mileage. The IRS considers a log to be timely if it’s updated weekly. The log should contain details of each business and personal trip, including:

- Date

- Mileage

- Destination

- Purpose

You should also log your total mileage for the year; read your odometer at the start and the end of the year. A mileage tracking app could be a handy tool for logging, record-keeping, and reporting all your business driving more swiftly and accurately.

Check out: The IRS free mileage log template [download in PDF, Excel or Sheets formats]

For a full breakdown of what the IRS considers adequate records — including the contemporaneous rule and what happens in an audit. See how to keep an IRS-compliant mileage log.

For the actual expenses method

As with the standard mileage rate method, you need to keep a timely log of your mileage (see above).

In addition, you must maintain documentation and hold onto all receipts associated with owning and running your vehicle to claim actual expenses. Those include depreciation calculations or lease payment receipts, as well as receipts for all deductible expenses (listed above).

To help you maintain all the records accordingly, download our free income & expense spreadsheet.

How to calculate your 1099 mileage tax deductions

The standard mileage rate method

Example: Let's say you drove 2,000 miles for business in 2025.

To calculate your mileage tax deduction, multiply the 2025 mileage rate by your business miles. In this example, 2000 miles X $0.70 = $1,400 in mileage deductions.

The actual expenses method

If you drive your vehicle for business 40% of the time, you can claim 40% of your vehicle’s actual expenses for the year.

Example: Your mileage log shows you drove 2,000 business miles and 3,000 personal miles in 2025. You have kept all relevant invoices and receipts, and your expenses add up to $5,000.

First, you find the percentage of business-related driving. 2,000 miles out of the total 5,000 is 40%. This means you can deduct 40% of all car-related costs you had throughout the year. 40% of $5,000 is $2,000 in mileage deductions.

See which forms you have to fill out for your 1099 mileage deduction by either of the two methods in our how to claim mileage on taxes guide.

What the deduction actually saves you

The mileage deduction is more valuable than most self-employed people realise, because it reduces two separate taxes, not just one.

When you're self-employed, you pay income tax on your net profit, plus self-employment tax (SE tax) of 15.3% on top, which covers your Social Security and Medicare contributions. Your mileage deduction reduces your Schedule C net profit, which means both taxes go down.

Here's what that looks like at different mileage levels for 2026:

|

Business miles driven |

Standard mileage deduction |

Approximate total tax saved (at 30% combined rate) |

|---|---|---|

|

5,000 miles |

$3,625 |

~$1,088 |

|

10,000 miles |

$7,250 |

~$2,175 |

|

15,000 miles |

$10,875 |

~$3,263 |

|

20,000 miles |

$14,500 |

~$4,350 |

The 30% combined rate is an approximation — your actual saving depends on your tax bracket and SE tax position. But the SE tax component alone saves roughly 15 cents per dollar of deduction on top of your income tax saving. For high-mileage drivers, that difference is significant.

Use the mileage reimbursement calculator to estimate your deduction for 2025 or 2026.

Mileage tracking and your quarterly estimated taxes

If you expect to owe at least $1,000 in tax after withholding and credits, the IRS requires you to make quarterly estimated tax payments using Form 1040-ES. Most self-employed people who earn a meaningful income from their business will meet this threshold.

Your mileage deduction connects directly to these payments. Because the deduction reduces your Schedule C net profit, tracking miles accurately throughout the year lets you calculate a more accurate quarterly payment — rather than overpaying each quarter and waiting for a refund at filing time.

If you're tracking miles in real time, you can adjust each quarterly payment as your deduction grows, keeping more cash in your account during the year.

Driversnote shows your running deduction total as you log trips, so you always know your current deduction figure when it's time to calculate a quarterly payment.

Other circumstances for workplaces and vehicle ownership

If your home is your workplace

You can deduct business mileage if you have a home office that qualifies as your regular workplace and drive between your home and another work location in the same trade or business.

If your home isn’t your regular workplace, driving between home and work is considered a commute and isn’t deductible.

If you have no regular workplace

You can deduct mileage for business-related trips between your home and temporary workplaces outside of your metropolitan* area. Trips between your home and temporary workplaces in your metropolitan area are considered commuting miles, and you also can’t deduct them.

*A metropolitan area includes the area of your city's limits and the suburbs that are a part of that area.

If you operate a carpool

You can’t deduct the cost of using your car in a non-profit carpool. The payments you receive from passengers are considered a reimbursement for your car expenses.

When you run a carpool for profit, you must include the payments you collect from passengers in your income. You can then deduct your car expenses for those trips.

FAQ

Tired of logging mileage by hand?

Effortless. IRS-compliant. Liberating.

IRS Mileage Guide

- For Self-Employed

- For Employees

- For Employers

- Mileage Log Requirements

- How To Claim Your Mileage On Taxes In 5 steps

- Calculate Your Reimbursement

- Is Reimbursement Taxed?

- Current Mileage Rates

- Historical IRS Mileage Rates

- IRS Medical and Charitable Mileage

- California Mileage Reimbursement

- Standard Mileage Rate vs. Actual Expense Method: Which is Right for You?

- How is the IRS Mileage Rate Calculated